2Jour Gazette | Edition 2 | 29 Sept - 5 Oct 2024

- Marina 2Jour

- Oct 6, 2024

- 19 min read

Welcome to this week’s edition of 2Jour Gazette—your curated look at what’s been making waves in fashion and luxury. From the dockworkers’ strike that shook U.S. retail and supply chains to LVMH’s bold new partnership with Formula 1, there’s plenty to dive into. We’ll also take a closer look at Bottega Veneta’s fragrance debut—yet another luxury brand embracing the growing perfume trend—and check in on the latest financial updates as Nike faces challenges across key markets in Q1.

This week’s edition also brings you the latest business moves, including LVMH’s sale of Off-White™ and the much-anticipated ruling on Tapestry’s Capri takeover. On top of that, rumors of Net-a-Porter’s acquisition are swirling once again. And the creative world? It’s buzzing as Hedi Slimane’s sudden exit from Celine leaves a shake-up, swiftly followed by a new creative direction, while Missoni also sees a change in leadership.

Plus, I’ll be reflecting on fashion weeks, sharing my thoughts on why they felt a bit lazy. I went searching for answers in the financial reports of luxury brands over the past 10 years, and some of the numbers honestly surprised me. For example, how much of Saint Laurent's profits in 2023 came from bags? And what about Hermès? All the answers are here!

So, grab your favorite espresso (or perhaps a glass of champagne), settle in, and let’s explore the chic, the influential, and the simply fascinating moments from the past week.

x Marina 2Jour

45,000 Dockworkers Walk Out: The Strike That Shook U.S. Retail

This past week, a dockworkers' strike at key East and Gulf Coast ports caused major disruptions in U.S. supply chains, affecting retailers and fashion brands during the critical run-up to the holiday season. The strike began on October 1, 2024, after negotiations between the International Longshoremen’s Association (ILA) and the U.S. Maritime Alliance (USMX) broke down over wages and working conditions, involving over 45,000 dockworkers across 36 ports.

A tentative agreement was reached on October 3, following significant pressure from President Biden and acting Labor Secretary Julie Su, who mediated the talks. The deal, which includes a 60% wage increase over six years, ended the strike immediately and extended the expired contract until January 15, 2025. While operations at the ports have resumed, the economic ripple effects are expected to last for several weeks as businesses recover from the disruption.

This is particularly worrisome for multi-product retailers and fashion brands preparing for Black Friday, Cyber Monday, and Christmas sales.

Ah, I'm so not ready for Christmas time (Selfridges is more than ready)

LVMH Partners with Formula 1 in New 10-Year Deal, Replacing Rolex

As Formula 1 approaches its 75th anniversary in 2025, LVMH has been announced as a Global Partner in a 10-year agreement starting in 2025. The deal will involve several of LVMH’s key brands, including Louis Vuitton, Moët Hennessy, and TAG Heuer, replacing Rolex as Formula 1’s main luxury partner. LVMH itself named the partnership "historic".

The new LVMH partnership will officially begin at the start of the 2025 Formula 1 season and will merge the luxury group’s expertise with Formula 1’s focus on high-performance and innovation. As part of the agreement, LVMH’s Maisons will contribute to hospitality, limited-edition collaborations, and activations tied to Formula 1 events. Further details of the agreement will be announced in early 2025.

The sponsorship deal, valued at slightly more than $100 million a year, marks a fresh push by LVMH into the sports world. LVMH paid some 150 million euros ($165.77 million) to be the premium sponsor of the Paris Olympics (Reuters).

Stefano Domenicali, Bernard Arnault, Greg Maffei, Frédéric Arnault

The targeting of Formula 1 by LVMH comes as interest in the motorsport has surged in recent years, fueled by the expansion of race venues and the popular Netflix series ‘Formula 1: Drive to Survive.’

LVMH brands have been targeting sports for a while to expand their visibility, featuring tennis stars like Roger Federer, Rafael Nadal, and Carlos Alcaraz, as well as football legends Cristiano Ronaldo, Lionel Messi, and Kylian Mbappé in their campaigns. The latest collaboration is out right now—F1 driver Lewis Hamilton has joined Dior as a guest designer for a capsule lifestyle collection (your thoughts on the collection? Google Lens gives me Asos, Arket, Zara vibes).

Also since 2021, the Formula 1 Grand Prix de Monaco™ Trophy has been presented in a custom-made Louis Vuitton trunk, continuing the partnership between Louis Vuitton and the Automobile Club de Monaco.

Rolex, which had been Formula 1’s official timekeeping sponsor since 2013, has long been a prominent presence at F1 events, with its signature green and gold branding becoming a staple on racetracks. Losing this partnership is a notable change for the brand, which remains closely tied to other elite sports such as tennis and equestrian events.

Luxury Perfume Effect: Bottega Veneta’s Fragrance Debut

Bottega Veneta launched its first fragrance collection under Creative Director Matthieu Blazy, with all five perfumes, priced at €390 each, developed by the brand's new in-house beauty arm, which employs its own perfumers. This launch marks a significant milestone for Kering Beauté, as it represents the first fragrance collection developed entirely within the Kering group since the division was created in 2023 to capitalize on the growing luxury beauty market.

*Thanks, Bottega Veneta, for putting effort into bottle design—others often ignore the fact that it can be difficult to distinguish perfumes on a vanity and release them in identical bottles.

Kering Beauté was founded to extend the reach of its luxury Houses into beauty and fragrance, managing their own products instead of relying on third-party licenses. This move gives Kering more control over how their brands express themselves through beauty products, allowing them to fully leverage their heritage and values in the process.

Luxury perfumes have gained significant attention from brands. To keep my case study, "How to Sell Luxury Perfumes Online," relevant, I track new releases (nothing which I haven't mentioned in the case study). Latest include updates from Chloé, Balmain, Christian Louboutin, and Loewe (Loewe limited-edition perfume with caps, designed with Lladró, are among my faves, design matters).

Many luxury fragrances are managed under licensing agreements (the largest players include Puig, Estée Lauder and Coty). However, Kering Beauté’s in-house approach signals their focus on this growing and promising market. Why promising? You've probably heard of lipstick effect, a phenomenon where consumers continue buying small luxury items, like perfumes, even during economic downturns. Coined by Leonard Lauder, chairman of Estée Lauder, after noticing a spike in lipstick sales during the 2001 recession, it reflects how people still seek affordable indulgences to maintain a sense of luxury and comfort in tough times.

It seems that the "lipstick effect" has now transformed into a "luxury perfume effect". As of 2023, the global luxury perfume market is valued at approximately $12.6 billion and is expected to continue its growth, reaching $34.39 billion by 2030, with a compound annual growth rate (CAGR) of 6.2% from 2024 to 2030 (sourse). This increase is driven by rising demand for premium and exclusive fragrances, with many consumers turning to perfumes as an affordable luxury during economic uncertainties.

PROFIT WATCH: TRACKING FINANCIAL WINS AND LOSSES

Oh, the time is coming! We’re approaching the season when luxury and fashion brands, along with groups, are set to announce their third-quarter 2024 results.

Falling Behind: Nike’s Sales Drop Across Key Regions in 2025 Q1

01 Oct 2024. Nike, the brand behind inspiring mantra from last week's edition, has reported a 10% drop in revenue for the first quarter of fiscal 2025, with total revenues coming in at $11.59 billion, compared to $12.9 billion in the same period last year. Sales were down in key regions, including North America and Europe, both seeing a 14% decrease. The company's net income also fell by 28%, down to $1.05 billion, with earnings per share dropping from $0.94 to $0.70.

Nike has been dealing with higher expenses, such as costs related to marketing (called demand creation expenses) and general overhead, which contributed to the decline. However, there was some good news: the company managed to reduce its inventories by 5% and continued to return money to shareholders through dividends and share buybacks, totaling $1.8 billion.

THE BUSINESS SHIFT BULLETIN: MERGERS, SALES & DIVESTITURES

LVMH Parts with Off-White™: Brand Sold to Bluestar Alliance

30 Sept 2024. LVMH isn’t just in the business of buying brands (their latest move being last week’s Moncler investment); they’re selling too. On what would have been Virgil Abloh’s birthday, LVMH announced that they’ve sold Off-White™—the brand’s parent company, Off-White LLC—to Bluestar Alliance, a New York-based brand management group. No financial details of the sale have been disclosed, but Off-White™ will now sit in Bluestar Alliance’s portfolio, alongside brands like Hurley, Scotch & Soda, Bebe, and Brookstone. Bluestar Alliance is known for managing brands with a strong department store presence, so it will be interesting to see how they steer Off-White going forward.

Just three years after taking a 60% control stake in the company in July 2021, LVMH decided it was time to part ways. Back then, they increased their stake to gain majority control, with the remaining 40% owned by British e-commerce player Farfetch, while Abloh retained the trademark rights. However, this sale brings added complexity: while LVMH owned the Off-White™ trademarks, the brand’s operating company, in which LVMH held a minority stake, still has a licensing agreement in place with New Guards Group, owned by financially troubled Farfetch. This licensing deal is up for renegotiation next year.

The sale comes shortly after Off-White™ secured a basketball partnership with the NBA, a move led by CEO Cristiano Fagnani. The partnership was part of Fagnani’s strategy to reconnect the brand with its roots in street culture, a key component of Abloh’s original vision for Off-White™.

Merger Showdown: Judge to Decide Fate of Tapestry’s Capri Takeover

The U.S. antitrust trial over Tapestry's $8.5 billion acquisition of Capri Holdings has concluded, with a decision now pending from a federal judge. The merger, announced in August 2023, would combine Tapestry's brands—Coach, Kate Spade, and Stuart Weitzman—with Capri’s brands—Versace, Michael Kors, and Jimmy Choo. This deal is seen as a major consolidation in the luxury and affordable luxury markets, but it quickly faced opposition from the Federal Trade Commission (FTC), which argued that the merger could reduce competition and harm consumers in the handbag market.

The FTC, tasked with protecting consumers and maintaining fair competition, halted the deal shortly after its announcement, leading to the current trial. Throughout the case, both sides have argued over the definition of accessible luxury and the potential impacts on pricing and consumer choice. The FTC is particularly concerned that the combined entity could dominate the affordable luxury handbag market, limiting options for consumers.

Executives from both Tapestry and Capri have testified during the trial, defending the merger as a strategic move that will enhance competitiveness against other luxury giants, such as LVMH and Kering. With fashion markets evolving rapidly, the companies argue that consolidation is key for survival and growth in global markets.

The court’s ruling will decide whether the merger can proceed or if it will be permanently blocked. The decision is expected in the next three weeks to three months.

Mulberry Drama: Final Act or To Be Continued?

Mulberry, known for it bags in 2000s have left his best times behind and is now struggling. It has been a long time since the brand came into my focus, but this week was news-making—enough to write an engaging chapter for The Business Shift Bulletin:)

This past week, Mulberry rejected an £83 million takeover bid from Frasers Group, which currently holds a 36.9% stake in the company. Frasers also announced plans to acquire an additional 4 million shares, slightly raising its stake to up to 37.3%—still far from gaining majority control.

Kate Middleton, Kate Moss, Alexa Chung with Mulberry bags

Mulberry, dealing with a 4% revenue decline and a £34.1 million loss for the year ending March 2024, has initiated a £10 million capital raise.

Additionally, Ong Beng Seng, linked to major shareholder Challice, was charged in Singapore in a corruption case.

With Frasers having until October 28 to make a formal offer or withdraw, Mulberry's future remains uncertain as it navigates these financial and strategic challenges.

Frasers Group, which owns Sports Direct and House of Fraser, acquired MatchesFashion (or now simply Matches) on 20 December for £51.9m. They then placed it into administration on 8 March. The retailer is now closed—I took this picture with flag down just a few days ago while passing by their former office in Mayfair, which I once attended for an event.

London <3

Richemont’s Exit? Mytheresa Eyes Net-a-Porter. Again.

Speaking of Matches, I can’t help but mention the latest (or not-so-latest) rumor about a potential acquisition of YNAP Group (which includes Net-a-Porter and Mr. Porter) by Mytheresa. YNAP is currently a loss-making asset for Richemont, and these rumors about a possible deal have surfaced before.

Combining Mytheresa and Net-a-Porter could create an ideal synergy. Net-a-Porter could improve Mytheresa’s technical appearance and content management, while Mytheresa could share its expertise in VIP customer (or Front Row loyalty program, how they call it). Front Row significantly contributes to Mytheresa’s stability and, looking at multi-brand e-commerce competitors, including Matches and Farfetch, I would say success, according to its latest revenue report.

My broad opinion on luxury e-retailers, including Net-a-Porter, Mytheresa, Matches (when it still existed), 24S, and Luisaviaroma, where I've been a VIP client, is here.

THE JOB SHIFT JOURNAL: HIRES, FIRES & TRANSITIONS

Rapid Turnover: Hedi Slimane Departs Celine, Successor Named in Hours

2 Oct 2024. Hedi Slimane has stepped down as creative director of Celine after seven years. During his tenure, Slimane injected new life into the brand, expanding into menswear, perfume, and beauty, and elevating Celine to become the third-largest fashion brand in the LVMH portfolio by revenue, more than doubling its performance (according to estimates, as LVMH doesn’t disclose specific figures).

Two rumors had been swirling for a while. First—there were rocky contract negotiations with LVMH. Second—Slimane was reportedly in talks with Chanel. As Andrea Batilla pointed out, Slimane wanted full control over all of Chanel’s divisions, including fragrance, but the Wertheimer brothers refused to grant him that level of authority.

The crashing 7th-century chandeliers in the setting of Slimane’s last Celine collection film now seem far more symbolic. The collection, without question, is my favorite of the season.

Events unfolded quickly (the ruthless world of fashion, or it’s just business—nothing personal? x). Just a few hours after the announcement of Slimane’s departure, Michael Rider was named as the new creative director of Celine.

Rider stepped down from Polo Ralph Lauren in May, where he had served as creative director for womenswear since 2018. Prior to that, he spent a decade at Celine under Phoebe Philo (2008-2018). Rider began his fashion career at Balenciaga in Nicolas Ghesquière’s atelier from 2004 to 2008.

Missoni’s Next Chapter: Grazioli Exits, Caliri Steps Up

3 Oct 2024. Filippo Grazioli is exiting Missoni after two years as creative director. Missoni CEO Livio Proli confirmed the “amicable” split, with Grazioli’s last show for Spring 2025 in Milan. Alberto Caliri, a longtime Missoni designer, will take over, debuting his first collection for pre-fall.

Caliri, who joined Missoni in 1998, previously led the brand’s home collection and served as interim creative director in 2021. Under Grazioli, Missoni revisited its iconic zigzag patterns, though rumors of his exit surfaced as menswear was taken over by an in-house team. His career includes working with Martin Margiela, Riccardo Tisci, and Burberry.

Missoni continues to expand globally, with 2% sales growth in the first half of 2024, driven by retail openings in Dubai, Spain, and Greece, and its home collection, which now accounts for 22% of total sales. Althogh for me Missoni is always about summerwear—nothing fits a vacation better than Missoni's cover-up x

Paris Fashion Week in a Flash

Fashion weeks are over, and it left me... oh... it left me disappointed. The most anticipated shows took place last week, and I have a lot to say.

Valentino. This collection by newly appointed Alessandro Michele was probably one of the most anticipated. We got a glimpse of what to expect with the Resort 2025 collection, and the Spring 2025 runway show continued in the same direction. I was truly captivated by broken glass floor, which added to the moody presentation, along with the white sheets on the lamps, which were part of the show's decor. Yes, it was truly a show, difficult to perceive as separate looks on the models, let alone individual pieces of clothing.

I've been following fashion shows for years, and I could sense the old Valentino, but even with an eye for detail, it was challenging. Alessandro Michele didn't bring Gucci to the Valentino runway, and I would even dare to say that he didn’t bring much of himself either, as many claim. What he did bring was a show. He brought overstyling, which distracted from each individual item in the outfits. The staging was the same way distracting—the models didn’t walk confidently like a true Valentino woman would. Instead, they floated like schoolgirls who had raided their mother’s wardrobe and put on everything all at once.

Oh, I truly hope the same overstyling doesn’t find its way to the Valentino website, like it once did with Gucci. Gucci has now moved to a clean interface with a focus on individual items, not outfits or fashion stories—and trust me, this is exactly what the customer needs in e-commerce.

Balenciaga. When the show just started, I was confused by the Dolce & Gabbana vibes—lace, stockings, flowing dresses. But that was just the introduction. After that, we saw the familiar outfits, as if thrown together from a pile of clothes at the nearest second-hand store.

It feels like Balenciaga has too much money for experiments with RTW.

Chanel. While the fashion crowd eagerly awaits the announcement of a new creative director, the brand presented a collection, created by the fashion house’s atelier, which could certainly use a breath of fresh air. Tik-tok.

Miu Miu. There was no magic (just like with the Prada show). Styling may draw your attention away from the individual pieces to the overall look, but in the end, each item will hang alone in a boutique. After the rapid growth in sales, nearly doubling in the first half of 2024, it will be very interesting to see the revenue for the full year (and for 2025 as well).

Relationships based on hype are usually short-term excitement, which doesn’t turn into long-term connections.

Louis Vuitton. I remember Nicolas Ghesquière from his tenure at Balenciaga, and I truly admire his talent. But not this time. Louis Vuitton had the models walk on a runway made of trunks, with leather goods seeming to be the main point of interest. Sadly. I visited a Louis Vuitton boutique a while ago and tried on a lot of pieces (which haven’t made it to the 2Jour Stylist lookbook platform), and I would never have thought—especially after watching the latest runway show—that this brand actually has nice, wearable ready-to-wear.

The Row may not want us to talk about it, hah, and the guests at the show couldn't take pictures again. But the collection has now landed for a preview, and it’s the opposite of almost everything (unwearable) I've seen this season. Simple, basic, high-quality (I hope with that price point, as I’ve never tried anything from The Row). Something the current luxury fashion market lacks—an easy (but not for everyone) formula to secure investments from the Wertheimer brothers, who control Chanel, and Françoise Bettencourt Meyers, granddaughter of L’Oréal founder Eugène Schueller, who recently bought minority stakes in The Row in a funding round that values the company at $1 billion.

There are two words I could use to describe the SS25 collections. First—"archival"—as many designers went back to their roots. Some interpreted them quite literally, while others re-imagined the archives with contemporary elements.

The second word is "(un)wearable." Major brands seem uninterested in ready-to-wear, giving the impression that either creative directors are tired or have been given free rein to bring their wildest ideas to life. And I must say, that wild side is the one with "un" at the beginning.

In trying to interpret this aftertaste, I went through the financial reports to find answers.

In Figures: Which Category Really Matters in Luxury Fashion

If you’ve been wondering (like I did) why the SS25 runway collections seemed to be lazy, it might be because the true driving force behind luxury brands lies elsewhere. Certain categories consistently generate the highest revenues, overshadowing the creative allure of ready-to-wear. By exploring the financial reports of luxury groups and brands over the last 10 years, I discovered what truly sustains these brands beyond the runway. Well, that was no wonder, as I've noticed the tendancy with e-commerce display earlier. Anyway, let's take an in-depth look.

So, which categories support powerhouse brands, and how do they shape the luxury landscape beyond the catwalk?

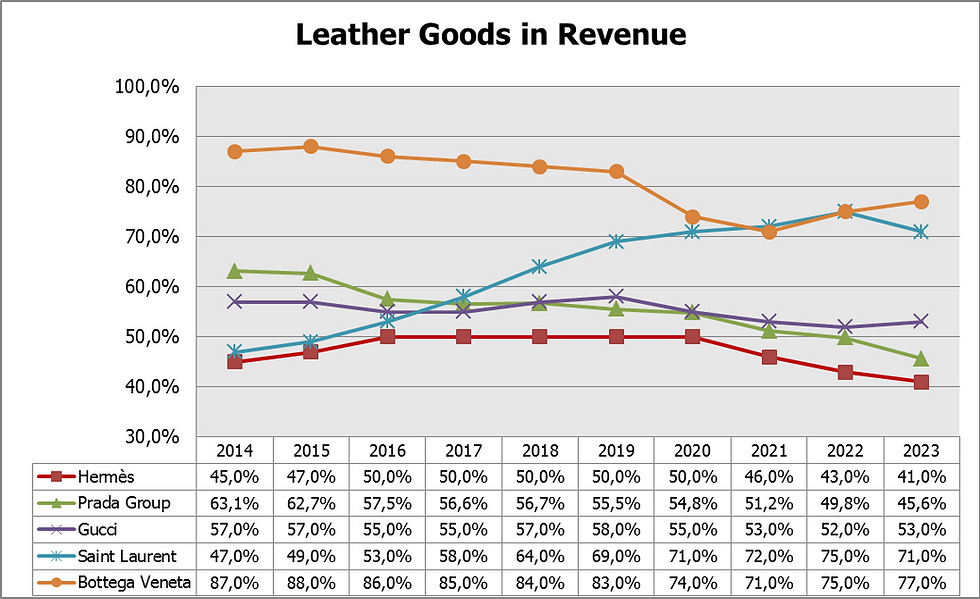

Luxury brands are still heavily reliant on Leather Goods as their main source of revenue, while Ready-to-Wear (RTW) and Footwear contribute a much smaller share. Leather goods have remained the cornerstone of luxury brand revenues over past 10 years, and although some brands are working to diversify into fashion and footwear, this shift is happening more gradually for some than others.

Heavy Reliance on Leather Goods:

Saint Laurent is a prime example, where 71% of its revenue still comes from leather goods in 2023, with only 20% from RTW & Footwear.

Bottega Veneta remains similarly dependent, with 77% of revenue generated by leather goods in 2023, reflecting a clear focus on accessories and leather craftsmanship.

Brands Moving Toward Diversification:

Prada Group has made significant strides toward diversifying its revenue streams. Leather goods now contribute 45.6% of its total revenue (down from 63.1% in 2014), while RTW & Footwear have grown to 50.7%, showcasing Prada’s increasing investment in fashion collections.

Hermès, while still leather-focused, has balanced its portfolio better than most. Its RTW & Footwear segment has grown to 29% in 2023, showing steady diversification while still leveraging its heritage in leather.

So, while on one hand, it explains why brands might not be putting their greatest effort into RTW and footwear, on the other hand, the runway is still the place to make a splash and win the race for the customer’s attention (and wallet). After all, the sleek and simple suit worn by Bella Hadid at Saint Laurent garnered the highest number of preorders in years (insider info), proving that clothing can still rock the fashion scene.

In-Depth | Power categories within the brands

We'll start with LVMH. Just kidding:) As you may know, LVMH doesn’t disclose the revenues for each of its individual brands, nor does it provide a detailed category breakdown within each maison family.

Kering does. At Gucci, leather goods remain the largest revenue contributor, accounting for 53% in 2023. This represents a slight decline from 57% in 2014, indicating a gradual decrease in the dominance of leather goods over the years. While still the core of Gucci’s business, this category has become slightly less central as other product lines have gained importance.

Ready-to-wear has seen a modest increase over the same period. In 2014, it contributed 12% of revenue, and by 2023, this figure had grown to 15%. Although it still accounts for a smaller portion of the overall revenue, the steady growth suggests that Gucci’s ready-to-wear collections are gaining more traction.

Shoes have shown significant growth, rising from 14% of revenue in 2014 to 20% in 2023.

Gucci’s revenue mix has become more diversified over the last decade. While leather goods remain the biggest contributor, their share has slightly declined. At the same time, ready-to-wear and shoes have steadily gained importance, with shoes, in particular, showing a notable increase in revenue share. This trend highlights Gucci's shift toward a more balanced portfolio, responding to broader luxury market dynamics.

At Saint Laurent, leather goods are also the biggest revenue contributor, accounting for 71% in 2023. This represents a significant increase from 47% in 2014, showing that leather goods have become even more central to the brand's overall revenue. Unlike Gucci, where leather goods saw a slight reduction, Saint Laurent has leaned heavily into this category, making it the core of their business.

Ready-to-wear, on the other hand, has seen a decline over the same period. In 2014, it contributed 24% of the revenue, but by 2023, its share had dropped to 12%.

Shoes accounted for 8% of revenue in 2023, a small but consistent contributor that has seen a slight decline from 19% in 2014. This steady decrease indicates that shoes, while important, are not as central to Saint Laurent strategy.

Saint Laurent's revenue has become increasingly concentrated in leather goods, which have grown significantly in share over the past decade. In contrast, both ready-to-wear and shoes have seen declining importance, signaling a clear strategic pivot toward higher-margin leather products.

Bottega Veneta. Leather goods remain the dominant revenue driver, contributing 77% in 2023, down from 87% in 2014. Despite a slight decline, this category far outweighs the others, cementing its central role in the brand's profitability.

Ready-to-wear has gradually increased its share, rising from 5% in 2014 to 10% in 2023, indicating a steady but modest focus on expanding fashion collections.

Shoes have also grown, from 6% to 10% over the same period, with a notable spike to 16% in 2020. While both categories have seen positive trends, their contributions remain minimal compared to the overwhelming dominance of leather goods.

The data proves Bottega Veneta is heavily reliant on leather goods, with modest growth in RTW and shoes.

In Kering portfolio Gucci stands out as the most balanced brand, with a significant contribution from leather goods but also considerable revenue from ready-to-wear and shoes. Its diversification makes it more resilient to market shifts and trends, especially in RTW. Bottega Veneta and Saint Laurent are both highly dependent on leather goods, with minimal diversification. Although both brands have seen some growth in RTW and shoes, their revenue remains skewed toward leather products, and ready-to-wear plays a smaller role.

You may be surprised, but Hermès has more diversified and balanced revenue mix. Or maybe it is the result famous catch-me-if-you-can game? x

Leather goods remain the largest revenue driver for Hermès, though its contribution has gradually declined. In 2023, leather goods made up 41% of revenue, down from 50% between 2016 and 2020. While still the backbone of the brand, this decrease suggests a shift towards diversification into other categories.

Ready-to-wear & Accessories, which include ready-to-wear clothing, fashion jewelry, hats and gloves, belts, and shoes, have seen substantial growth. In 2023, they contributed 29% of total revenue, up from 23% in 2014. This increase signals Hermès' expanding focus on the fashion segment, as these products now play a significant role in the brand's overall revenue mix, second only to leather goods.

Hermès has significantly diversified its revenue streams, with ready-to-wear and accessories (including fashion jewelry, hats, belts, gloves, and shoes) becoming an increasingly important contributor alongside leather goods. While leather goods still dominate, their share has declined as Hermès strengthens its presence in the fashion and lifestyle segments. Who knows, maybe couture is closer than we think x

At Prada Group RTW has shown consistent growth, rising from 16.9% of revenue in 2014 to 32.2% in 2023. This demonstrates Prada's strategic focus on expanding its clothing collections, which has become a key revenue driver.

Leather Goods, once Prada’s dominant category, have seen a significant decline. In 2014, this segment represented 63.1% of total revenue, but by 2023, it dropped to 45.6%, indicating a shift away from heavy reliance on traditional leather products.

Footwear has remained stable, contributing around 18-19% of revenue. It accounted for 18.3% in 2014 and 18.5% in 2023, peaking at 21.6% in 2016.

Prada Group's business is diversifying, with Ready-to-Wear becoming increasingly important, while Leather Goods has decreased. Footwear remains steady but hasn’t experienced significant growth.

Stay tuned for the next week edition x