2Jour Gazette | Edition 5 | 21 Oct - 27 Oct 2024

- Marina 2Jour

- Oct 28, 2024

- 9 min read

Welcome to this week’s edition of 2Jour Gazette—your curated look at what’s been making waves in fashion and luxury. This week marked a continuation of Q3 2024 earnings reports, and while luxury fashion still faces a notable slowdown—especially with Kering showing the biggest sales drop—there are brands that continue to report growth.

Hermès. I flipped through page after page of the latest edition of Le Monde d'Hermès, the brand’s regular publication. Although I’d seen mentions of newsstands worldwide before, I never paid much attention—this is the first issue I've had in my hands. Many publications and blogs often recount archival stories of luxury brands or their iconic elements. It’s funny, as it's the brands themselves who are most interested in these stories—they strengthen the emotional connection. Yet, I often note that in the endless rush of aggressive marketing or influencer partnerships, fashion houses overlook this crucial nuance, which not only serves as a logical extension of client engagement but is also relatively inexpensive. Brands have stopped telling stories, making it easy for consumers to switch labels without emotional attachment. Speaking of labels, Hermès skillfully integrates storytelling and heritage into its unique marketing, so much so that the evolution of its approach was illustrated in the latest issue.

This edition is all about numbers. There were so many that even I got a bit overwhelmed, but to simplify your journey through the data, I’ve added a few tables and charts. Besides the reports, this issue also includes two noteworthy updates. The first involves the long-standing drama over the (unsuccessful) Tapestry acquisition of Capri Holdings. The second is Estée Lauder’s entry onto the Amazon platform, specifically for its luxury lines. Beauty brands often avoid Amazon to protect their premium image, but Estée Lauder’s move has a clear rationale, which I’ve explained in the news piece.

So, grab your favorite espresso (or perhaps a glass of champagne), settle in, and let’s explore the chic, the influential, and the simply fascinating moments from the past week.

x Marina 2Jour

• Zegna Reports 8% Q3 Revenue Drop

• Luxury Market Challenges Hit Kering, Reporting 15% Drop in Q3 Revenue

• Resilient Hermès Sees 11% Revenue Boost in Q3 2024

• L'Oréal Q3 2024 Sales Rise 6%

• Beauty and Ice Cream Drive Unilever's 4.5% Q3 Revenue Increase

• FTC Halts Tapestry’s Ambitious Merger with Capri Holdings

Estée Lauder Partners with Amazon, Launching Luxury Beauty on U.S. Platform

22 Oct 2024. Estée Lauder has announced its expansion to Amazon, focusing specifically on the United States market. This strategic move aims to tap into the growing U.S. e-commerce sector. The partnership marks the first time Estée Lauder's high-end beauty and skincare products will be available on Amazon’s U.S. platform, reflecting a shift in the company’s digital strategy. This decision targets a broader audience, particularly younger consumers and online shoppers who favor the convenience of major e-commerce platforms.

By leveraging Amazon’s vast logistics network and digital reach in the U.S., Estée Lauder expects to boost its online presence and adapt to changing consumer habits that increasingly favor digital purchases over traditional retail. The move is part of a broader industry trend where luxury and premium brands are opening up to e-commerce platforms to capture market share while maintaining a focus on authenticity and brand image.

Estée Lauder's collaboration with Amazon will include a curated selection of products specifically for the U.S. market to maintain its luxury appeal. This step aligns with the company’s goal to expand its digital footprint in the United States and drive sales growth in a competitive and evolving beauty market.

I also see this move as an attempt to capture a larger market by offering customers different ways to purchase products online. The search can be brand-targeted, where the consumer is looking for a specific brand or product, or it can be more general, focusing on finding an item to meet a current need without a clear brand preference. In this particular case, the latter is implied.

PROFIT WATCH: TRACKING FINANCIAL WINS AND LOSSES

Zegna Reports 8% Q3 Revenue Drop

22 Oct 2024. For the first nine months of 2024, Zegna's total revenue reached €1.36 billion, showing a 2% increase year-on-year (YoY) at constant exchange rates, but a 4% decline in organic growth. Q3 revenue was €397 million, marking an 8% decrease YoY.

By brand:

Zegna: Slight growth with a 3% organic increase, largely due to strong Direct-to-Consumer (DTC) sales in Europe, the Americas, and Japan;

Thom Browne: Declined by 27% organically, impacted by the wholesale channel and weaker performance in Greater China;

Tom Ford Fashion: Showed mixed results, with an 11% organic decline overall, though the DTC segment grew 3%.

By Geography:

EMEA: 2% organic decrease, with mixed performance between brands;

Americas: 3% organic decline, mainly due to timing differences in wholesale deliveries;

Greater China: Significant 22% organic drop, reflecting consumer uncertainty;

Rest of APAC: 7% organic growth, with positive trends in Japan and Korea.

See the full presentation here.

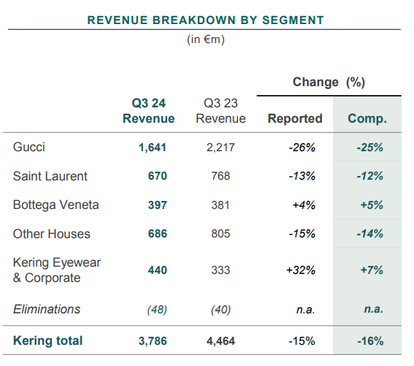

Luxury Market Challenges Hit Kering, Reporting 15% Drop in Q3 Revenue

23 Oct 2024. Kering reported Q3 2024 revenues, confirming deepening challenges in the luxury market.

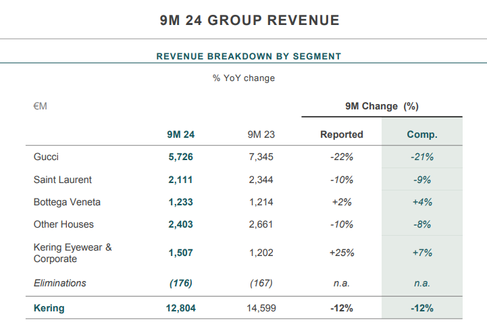

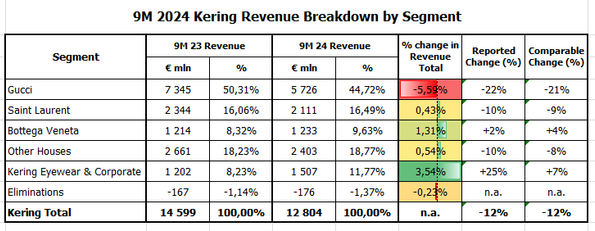

The total Q3 2024 revenue was €3.79 billion, reflecting a 15% reported decline and a 16% comparable drop. Most segments declined, including Gucci (-25%), which accounted for 43.34% of Q3 2024 and 44.72% of 9M 2024 group revenue. However, two areas showed slight growth: Bottega Veneta and Kering Eyewear & Corporate.

Bottega Veneta was highlighted as a bright spot in the report, showing 5% growth in Q3 2024 and 4% in 9M 2024. It accounted for 9.63% of Group revenue in 9M 2024, reflecting a 1.31% year-over-year increase.

In Q3 2024, Kering's revenue performance showed distinct trends across different channels. Retail, including e-commerce, made up 75% of the group’s revenue but faced a significant 17% decline. Despite this drop, the company saw an expansion in its directly operated stores, reaching a total of 1,816, with a net increase of 15 stores compared to June 2024. It was mentioned during a Q&A session that Kering plans to re-evaluate the existing store network, potentially closing locations with less impact to reduce expenses. The same approach will apply to digital investments, with a focus on developing the existing digital base.

Wholesale and other channels, representing 25% of the group’s revenue, experienced a 12% decrease overall. Within this segment, wholesale luxury brands saw a notable decline of 27%. However, there were areas of growth: Kering Eyewear & Beauté's wholesale segment grew by 5%, and Royalties & Other revenues increased by 18%.

Kering's retail revenue showed regional variations, with Western Europe experiencing an 11% decline, reflecting consistent negative trends across recent quarters. North America faced a steeper drop of 15% compared to previous quarters. In Japan, revenue growth slowed significantly, increasing by only 3% after stronger performances earlier in the year. The Asia Pacific region struggled the most, with a substantial 30% decrease, highlighting ongoing challenges. Meanwhile, the Rest of the World (RoW) showed slight resilience, growing by 2% in Q3.

When looking at the overall revenue breakdown by region, Western Europe remains the largest contributor at 32% of total revenue, up by 2 percentage points year-on-year. North America follows with 23% of revenue, also increasing by 2 points. The Asia Pacific, despite challenges, still holds 29% of total revenue, although it decreased by 5 points. Japan and the Rest of the World each contribute 8% to the group’s revenue, with both regions experiencing a 1-point increase compared to last year.

Key insights from the revenue presentation, and following QA session are:

Market trends

Declining demand: Consumer interest in luxury goods continues to weaken, with notable drops in Asia-Pacific.

Selective growth: Iconic products and high-end leather goods are performing better, showing resilience in a challenging market.

Strategy focus

Brand appeal: Emphasis on boosting desirability through iconic items, especially in resilient segments.

Cost efficiency: Plans to optimize existing store networks and manage operational expenses tightly.

Targeting high-end consumers: Continued expansion into luxury segments to capture wealthier client bases.

Forecast

Profit outlook: Kering aims for an FY24 EBIT of around €2.5 billion, despite cautious consumer sentiment and tightening costs.

Explore more in presentation and press-release.

Resilient Hermès Sees 11% Revenue Boost in Q3 2024

24 Oct 2024. Hermès delivered strong Q3 2024 results, highlighting resilience amid global challenges in the luxury sector. Total revenue increased by 11.% in the third quarter at constant exchange rates, contributing to a 13.8% rise over the first nine months.

Hermès reported strong growth across most sectors, except for Watches. Leather Goods increased by 17% due to high demand for both classic and new models, while Ready-to-Wear and Accessories rose by 15%, driven by positive reception of recent collections. Silk and Textiles showed modest growth at 2%, and Perfume and Beauty climbed 7%, with successful product launches. In contrast, the Watches segment declined by 6% due to high comparison benchmarks. Other Sectors, including Jewelry and Home, surged by 17%, reflecting growth across various categories.

Regionally, Japan led growth with a 23% increase, driven by loyal local consumers, while Asia-Pacific saw a more modest 7% rise, impacted by weaker performance in Greater China. The Americas and Western Europe maintained solid growth, with increases of 13% and 18%, respectively, indicating steady demand despite broader economic pressures.

Key insights from the update:

Hermès is expanding leather goods production with a new workshop in France, maintaining a focus on traditional craftsmanship and high-quality materials. This aligns with blending classic designs with new items;

The brand prioritizes growth in sectors like jewelry, home, and beauty while acknowledging challenges in the watch category due to last year's strong comparison base;

Hermès plans to continue leveraging its craftsmanship and iconic products, expecting steady demand in established categories while closely monitoring market conditions, especially in regions with fluctuating consumer sentiment.

See the brand quarterly information report here.

While the luxury segment is facing a significant slowdown, I consider Hermès to be more stable, as their primary focus is on clients who are more resilient to macroeconomic conditions, and the percentage of aspirational customers is lower. However, even this did not protect the brand from a plato in sales in the Asia-Pacific region (excluding Japan, which has been a strong point for every luxury group this Q3 season). This is due to the challenging economic environment, particularly in China, which I mentioned here.

L'Oréal Q3 2024 Sales Rise 6%

22 Oct 2024. L'Oréal Q3 2024 results showed a 6% increase in sales, reaching €32.4 billion for the first nine months of 2024. Growth was observed in all divisions, except for North Asia, where challenging conditions impacted performance.

By division:

Professional Products: Up by 5.8%, driven by innovation in haircare and omnichannel strategies.

Consumer Products: Grew by 6.4%, with strong performance in emerging markets.

L'Oréal Luxe: Rose 3.4%, supported by double-digit growth in fragrances.

Dermatological Beauty: Increased by 11.3%, outperforming market trends, especially in skincare.

By region:

Europe: Strong growth at 9.3%, led by haircare and fragrances.

North America: Sales rose by 6.9%, bolstered by channel expansion.

North Asia: Faced a 3.0% decline due to weak demand in China.

Latin America and SAPMENA-SSA: Grew by 12.3% and 12.6%, respectively, with strong performance in skincare and fragrances.

Key developments:

The acquisition of a 10% stake in Galderma to enhance dermatological expertise.

Expansion in sustainable beauty ingredients and technological innovations.

Positive momentum in both value and volume, with a focus on online channels, especially in emerging markets.

L'Oréal "remains confident in continued growth despite global uncertainties, planning a "beauty stimulus" for 2025 (planned initiatives aimed at boosting the beauty market, focusing on innovation, product launches, and marketing strategies to drive growth and consumer demand).

See the report here.

Beauty and Ice Cream Drive Unilever's 4.5% Q3 Revenue Increase

Unilever reported a 4.5% underlying sales growth, maintaining turnover at €15.2 billion, flat compared to the previous year. Growth was mainly volume-driven, led by Power Brands like Dove and Magnum.

Segment performance:

Beauty & Wellbeing: 6.7% growth, driven by strong performances in skincare and premium innovations;

Home Care: 1.9% increase, with Fabric Enhancers growing double-digit;

Nutrition: Muted growth at 1.5% due to lower prices and market moderation;

Ice Cream: Achieved 9.8% growth, led by successful product launches.

Geographical insights:

North America: 7.4% growth, driven by strong volume;

Europe: 6.5% growth, despite slight price reductions;

Latin America: Moderate growth at 3.8%;

Asia Pacific Africa: More modest growth at 2.5%.

Outlook:

Unilever expects full-year growth between 3-5%, focusing on volume-driven expansion, with a targeted operating margin of at least 18%. Investment behind major brands is expected to increase, with continued emphasis on innovation and market adaptation.

See more information in presentation.

BUSINESS TRANSITION BULLETIN: MERGERS, SALES & INVESTMENTS

FTC Halts Tapestry’s Ambitious Merger with Capri Holdings

24 Oct 2024. Tapestry’s attempt to acquire Capri Holdings, a move valued at $8.5 billion, faced a significant setback this week when a U.S. federal judge ruled against the merger. This decision aligns with the FTC's concerns over potential antitrust issues, highlighting fears that the merger could limit competition and create a dominant entity in the accessible luxury market.

The merger was initially seen as a way for Tapestry to consolidate its position in the luxury fashion market, bringing together renowned brands like Coach, Kate Spade, and Stuart Weitzman with Capri’s portfolio, which includes Michael Kors, Versace, and Jimmy Choo. The acquisition was intended to create a powerful American counterpart to European giants like LVMH and Kering, allowing the combined entity to leverage shared resources, supply chains, and digital platforms.

The court's decision reflects broader regulatory trends, as governments increasingly scrutinize mergers and acquisitions in key industries, including fashion and luxury. Tapestry argues that the merger would have strengthened its ability to compete globally, provided cost efficiencies, and improved customer experiences through better product offerings. However, the FTC’s position underscores concerns about reduced competition and the potential for higher prices.

The ruling has brought uncertainty to Capri Holdings, as its brands face market pressures without the anticipated backing of Tapestry’s resources. In response, Tapestry announced its intention to appeal, prolonging the legal battle and leaving the future of the merger unclear. This case has implications for the market, potentially setting precedents for future deals and the level of regulatory scrutiny they may face.

The day after the ruling, Capri's stock price dropped by nearly 50%, while Tapestry's stock price rose by 13.5%.

Stay tuned for the next week edition x